As advancements in healthcare and lifestyle continue to extend our lives, people are faced with the prospect of longer and more fulfilling lives. While this is undoubtedly a cause for celebration, it also necessitates careful consideration and planning from a financial perspective. As people live longer, it’s essential to understand the implications for retirement planning and financial security in later years.

1. Longevity Risk

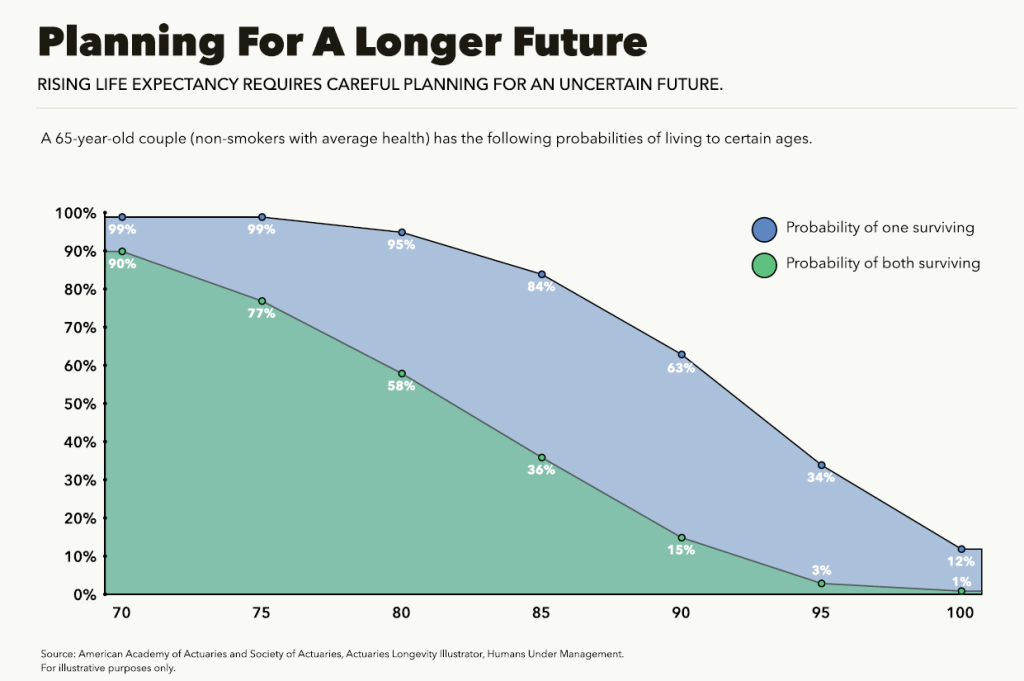

One of the primary financial considerations associated with increased lifespans is longevity risk – the risk of outliving your savings and resources. With longer life expectancy comes the need for a more extended period of financial support in retirement. People must plan for the possibility of living well into their 80s, 90s, or even beyond, ensuring that their financial resources can sustain them throughout their retirement years.

2. Retirement Savings

Building a robust retirement savings nest egg is essential for financial security in later life. Starting early and contributing regularly to pensions can help people accumulate sufficient funds to support themselves in retirement. Employers often offer workplace pension schemes, which provide an opportunity for employees to save for retirement with contributions from both the employee and employer. And the approaching auto enrolment will ensure everyone gets brought into a pension system.

3. Investment Strategy

Investing wisely is key to maximising returns and growing retirement savings over the long term. Diversifying investments across a range of asset classes, such as stocks, bonds, property, and cash, can help mitigate risk and capitalise on market opportunities. Individuals should consider their risk tolerance, investment objectives, and time horizon when developing an investment strategy tailored to their financial goals and retirement timeline.

4. Inflation and Cost of Living

As we’ve seen in recent years inflation erodes purchasing power over time, meaning that the cost of living tends to increase gradually. As people live longer, they must account for the impact of inflation on their retirement income and expenses. Planning for inflation by targeting growth can help protect against the eroding effects of inflation and ensure that retirees can maintain their standard of living throughout retirement.

5. Healthcare Costs

As individuals age, healthcare expenses tend to increase, particularly in later life when medical needs become more significant. Planning for healthcare costs in retirement is essential for maintaining financial security and peace of mind. Considering options such as private health insurance, long-term care insurance, and setting aside funds for medical expenses can help individuals cover healthcare costs effectively and mitigate the risk of financial strain in later years.

6. Estate Planning

Estate planning involves making arrangements for the transfer of assets and wealth to beneficiaries after death. As people live longer, estate planning becomes increasingly important for preserving wealth and ensuring that assets are distributed according to their wishes. Establishing a will, creating trusts, and considering inheritance tax implications are essential components of effective estate planning that can provide financial security and peace of mind for individuals and their loved ones.

Conclusion

As people enjoy longer lifespans, careful financial planning becomes paramount for ensuring a secure and comfortable retirement. By addressing longevity risk, building robust retirement savings, investing wisely, planning for inflation and healthcare costs, and engaging in estate planning, individuals can navigate the complexities of retirement with confidence and financial security. Taking proactive steps towards financial planning early in life can pave the way for a fulfilling and prosperous retirement in an age of increased longevity.